Backdoor Roth Checklist

⚠️ Surprising fact: Only 15-25% of eligible high income earners actually use the Backdoor Roth!

Who this is for:

High-income earners who are not eligible to deposit the maximum annual contribution directly into a Roth IRA on account of IRS income limits.

For the 2026 tax year, the maximum contribution to IRAs and Roth IRAs per individual is:

• $7,500 (under age 50)

• $8,600 (age 50 or older, including catch-up contributions)

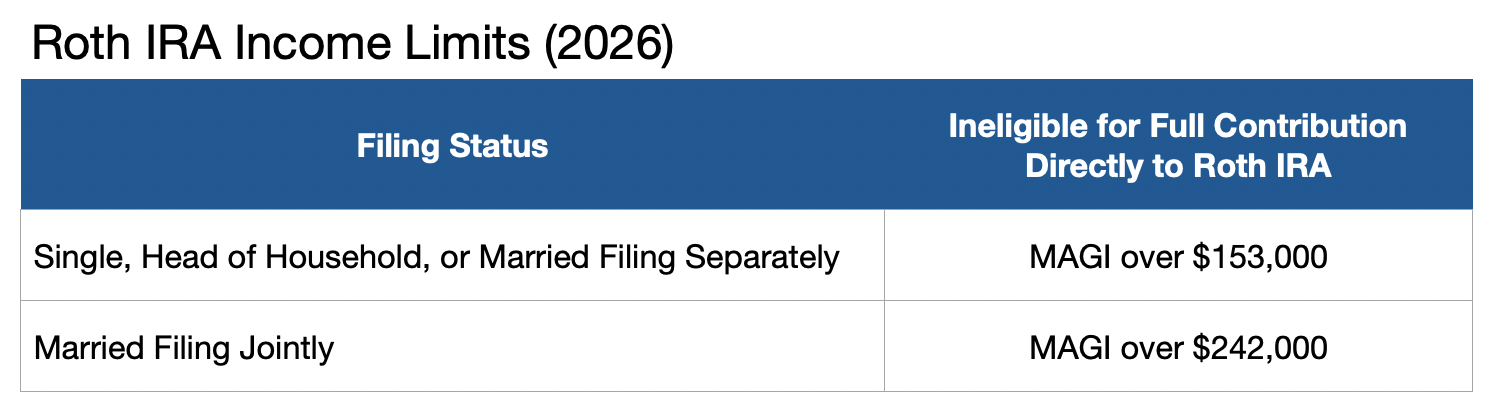

Step 1: Confirm a Backdoor Roth Makes Sense for You

Your income is above the Roth IRA income limits

You do not have pre-tax IRA balances as of December 31:

Traditional IRA

Rollover IRA

SEP IRA

SIMPLE IRA

⚠️ If you do have one of these, the strategy may still make sense for you — but it could require extra planning.

Step 2: Make a Non-Deductible IRA Contribution

Open a Traditional IRA (we set up a dedicated account for each client’s annual Backdoor Roth)

Contribute up to the annual IRA limit

Contribution is considered after-tax (non-deductible)

Funds are left in cash initially

Step 3: Transfer to a Roth IRA

Open a Roth IRA for use with your annual Backdoor Roth operations

Transfer the contribution from the Traditional IRA to the Roth IRA

Carry out the transfer soon after the contribution

The transfer is processed as a Roth conversion (not a withdrawal)

A few pennies of interest earned before conversion is acceptable*

Step 4: Invest Inside the Roth

Confirm Traditional IRA balance is $0

Roth IRA reflects converted funds

Invest according to your long-term investment plan

Step 5: Tax Filing (Critical)

Enter information from Form 1099-R into your tax return

File Form 8606 with your tax return

Contribution is reported as non-deductible

Conversion is reported correctly

Taxable amount is ~$0 (aside from minor interest, if any)

📄 Keep copies of Form 8606 permanently.

Step 6: Repeat Annually

Reconfirm eligibility each year

Check for new IRA balances before year-end

Repeat the process annually if appropriate

Good to know

Each spouse must complete this process separately

A non-earning spouse is not excluded from doing a Backdoor Roth IRA as long as the couple has sufficient earned income and files jointly

Contributions to a 401(k) retirement plan do not affect this strategy

Timing flexibility is allowed, but accuracy matters

*Tip: If a few pennies of interest are left over in the IRA, we ask our custodian to net them to zero.